Agile in an accountancy firm – recap

Agile is a project methodology. Agile is een projectmethodiek. Unlike traditional project methodologies, Agile does not have a tight hierarchy, no detailed long-term planning and no fixed budget. Agile is often applied in software development. At Braindumplabs we work agile as well.

In software development ‘scope creep’ is a mayor risk. Gradually, more and more functionalities are added to the list of requirements. Sometimes a part of the code is replaced by new requirements. Naturally, changes that are implemented last-minute have a negative effect on the budget. There is a Dutch parliamentary report regarding IT fails in government IT projects. In addition, continuous technological development means that specifications always change.

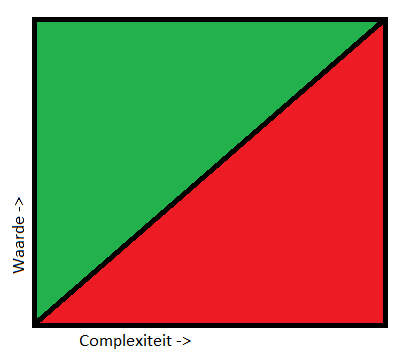

Software projects therefore have a tendency to run out of budget, be delivered delayed and ultimately not to the satisfaction of the customer. Agile offers a solution for this. The requirements are continuously updated. Only the most important and easily built functionalities are constructed as shown in the illustration. If a feature is very complex to build, this is only fulfilled if the value is high enough. Low-hanging fruit, easy to realize features that have a lot of value, are addressed first.

As a result, an Agile project has a positive atmosphere from the start. Results are quickly visible and give motivation for the follow-up.

Optimization of the work

This is an interesting interface with accountancy. Accountancy projects are more defined than software development. But the value for the customer is also more difficult to substantiate. Auditing is in many cases legally required. Obviously, a company benefits from audit. Internal procedures are reviewed. The auditor examens at the data management and cybersecurity threats. A auditor’s report provides the shareholders, bank and other stakeholders with certainty about the governance and continuity of a company. Yet not every organization is equally enthusiastic about the audit duty.

So if we apply the above sprint planning chart to the audit. The tasks with the most value and ideally least effort are executed first. Interim reports can be made about mitigated risk and recommendations for better internal control. When things go wrong in the project, parts of the audit appear to be more complex than previously estimated, the customer can be involved in the audit approach. Perhaps the complexity can be reduced or the value increased by switching from system-oriented to data-oriented approach, possibly with data analysis. The customer who can follow the progress of the project and receives a highlight report will have a better understanding of additional work or required additional information.

Changing specifications

Delay

An Agile software development project stops when the development costs no longer outweigh the value of the functionalities. An audit can not end when the budget runs out, or if the work in the eyes of the customer has no added value. The audit is legally required. And in the case of a voluntary check, there are requirements to the work of an accountant to come to a judgment. The project will therefore only end when the accountant can give an opinion on the annual accounts based on the work carried out. But by llinking value (mitigating effect of activities) and complexity (effort required), the audit can be viewed with a fresh perspective. If the risks are largely mitigated, a more efficient approach to the limited residual risk may be used to complete the assignment on time.

An agile approach, even if it is not formalized, will contribute to the successful completion of an audit. Employees are more effective and customers get more value for their audit fee. Do you want to know more about Agile? The upcoming blogs are about Agile, not the manifesto but about Agile rituals and traditions. Do you really want to take steps in working Agile? Please inquire about our workshop: Agile in the accountancy office.